Byond – An Innovative Approach to your Health Care

We are extremely excited to announce a new health resource available exclusively to SC Insurance clients. Byond is...

Read More

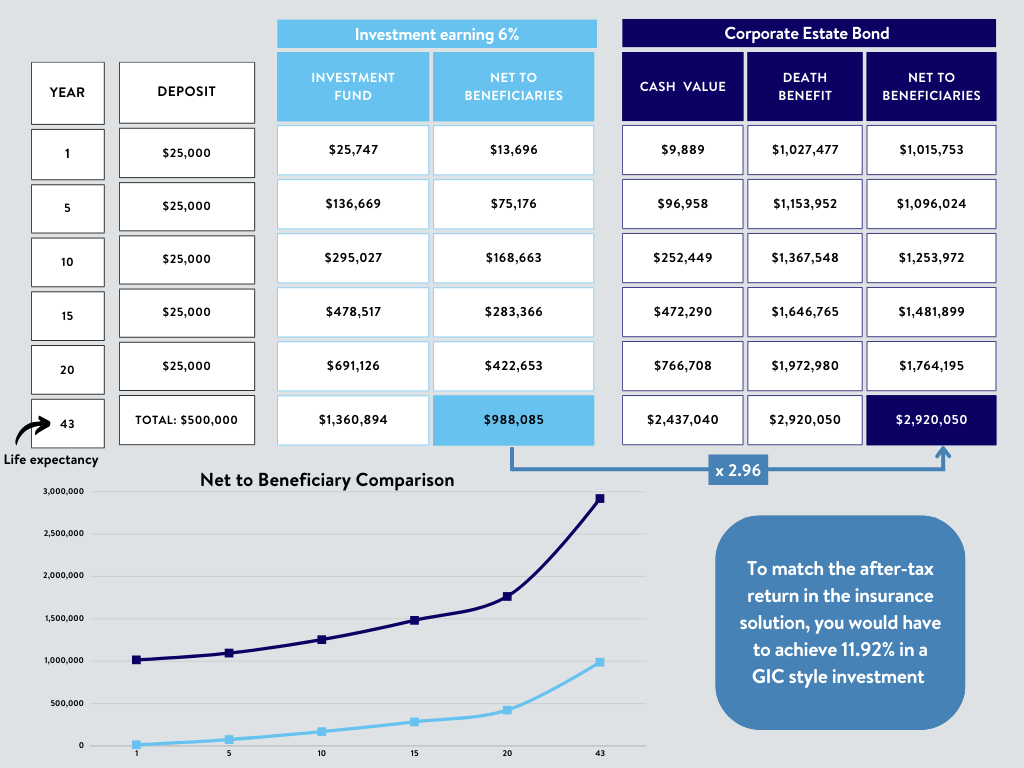

Your Estate Plan: Creating a Legacy, While Preserving Your Wealth

Many of our clients are reaching a new phase in their lives where they are thinking about their...

Read More

Life Insurance – Understanding your Options

Life insurance can be a complicated and often misunderstood product when not explained properly. Below is a brief...

Read More